The Settlement Offer That Arrives Before the Bruises Have Faded

She told me she almost signed. Three days after a rear-end collision on I-275, still taking ibuprofen every four hours, still sleeping on her side because her neck wouldn’t let her lie flat—and she was holding a release form and a check for $4,200. The adjuster had been warm, professional, quick to call back. He said the offer was fair given the circumstances. She said she felt guilty even hesitating.

That moment—the gap between the first offer and the first full medical evaluation—is where I spend most of my professional attention. Because what happens in that window can shape someone’s financial reality for years.

What Usually Happens in the First Week

The accident itself is disorienting enough. Then comes the paperwork, the rental car calls, the missed work, the icing and re-icing of whatever hurts. Most people are not thinking about claim strategy. They’re thinking about getting back to normal.

That’s exactly when the insurance adjuster calls.

The adjuster’s job is not adversarial in a theatrical sense—they’re not twirling a mustache. But their role is structurally misaligned with yours. They work for the insurer. Their performance metrics involve closing claims efficiently. And the fastest, cheapest close happens when the injured party hasn’t yet seen a specialist, hasn’t yet received imaging results, and hasn’t yet consulted anyone who explains what a claim release actually does.

The call is usually friendly. The offer sounds concrete. And for someone who is exhausted, in pain, and worried about bills, “concrete” feels like safety.

Here’s what that first offer typically reflects: the visible, immediate costs. Your ER copay. Maybe a few days of missed work if you mentioned it. The adjuster has your initial medical report—probably from urgent care or the ER—which documents acute symptoms but says nothing about what happens in week three when the headaches don’t stop, or month two when your orthopedist recommends an MRI that reveals a herniated disc that wasn’t visible on the original X-ray.

The offer is priced on what they know. Not on what’s coming.

The Costs That Haven’t Appeared Yet

This is where the real risk lives—and it’s worth slowing down here.

Soft tissue injuries—whiplash, muscle tears, ligament strains—are notoriously slow to declare themselves. The adrenaline of an accident masks pain acutely. Inflammation builds over days. Neurological symptoms from spinal involvement sometimes don’t appear for weeks. I’ve seen cases where the injured party felt “mostly okay” at day four and was in physical therapy three times a week by week six.

Consider the categories of cost that a day-three offer routinely ignores:

| Cost Category | What Adjusters Include | What’s Often Missing |

|---|---|---|

| Medical expenses | ER visit, urgent care copay | Specialist visits, imaging, future treatment |

| Lost wages | Days explicitly mentioned | Partial capacity work, contractor income loss |

| Out-of-pocket costs | Initial prescriptions | Follow-up MRIs, pain management referrals |

| Non-economic damages | Rarely addressed | Pain and suffering, functional limitations |

Future medical expenses are a legitimate, compensable part of your claim. The DOJ’s framework for personal injury compensation explicitly includes both current medical bills and anticipated future treatment costs, alongside non-economic damages like pain and suffering. An early offer almost never accounts for future care because the adjuster doesn’t have—and frankly doesn’t want—a specialist’s prognosis in hand before you sign.

Wage loss compounds quietly. Maybe you went back to work at partial capacity. Maybe your job involves physical demands you haven’t tested yet. Maybe you’re a contractor and the income disruption is harder to document but very real. None of that gets priced into a day-three offer.

And then there’s the category people least expect: the out-of-pocket costs that arrive after the settlement check clears. A follow-up MRI. A referral to a pain management specialist. A prescription that your health insurance doesn’t fully cover. Once you’ve signed a claim release, those bills belong entirely to you.

How the Adjuster Values Uncertainty—and Why That Works Against You

Insurance pricing is built on probability models. Adjusters understand this intuitively even if they don’t say it out loud.

When your injury picture is incomplete, the claim has uncertainty—and uncertainty is something insurers price to their advantage, not yours. If an adjuster offers you $4,200 before your specialist visit, and your specialist later documents $18,000 in future treatment needs plus significant functional limitations, the adjuster just saved their company roughly $14,000 or more. That’s not cynicism—that’s the structural logic of early settlement offers. Legal guidance from the American Bar Association is consistent on this point: personal injury lawyers routinely advise clients not to accept initial offers until the full extent of injuries is understood, precisely because early offers are made before future treatment needs are established.

The adjuster also knows something about leverage that most injured people don’t: your anxiety is working for them.

The fear that you’ll somehow miss your window, that the offer will evaporate, that waiting is greedy or risky—that fear is a negotiating asset for the insurer. It costs them nothing to let you sit with it. What’s actually true about timing? Florida’s statute of limitations for personal injury claims gives you meaningful time to make an informed decision. Filing deadlines by state vary, but most jurisdictions allow two to four years for personal injury suits—time that exists precisely so injured parties can understand what they’re dealing with before making permanent decisions. The offer won’t disappear if you take a few weeks to get a proper medical evaluation.

What a Claim Release Actually Means

A claim release is not a receipt.

It’s a legal document that typically extinguishes your right to pursue any further compensation from that insurer for that accident—permanently, regardless of what you discover later. The language is usually broad. “Any and all claims, known and unknown, arising from the incident described herein.” That phrase is doing serious legal work.

The injured party who signs on day three doesn’t know yet that they have a herniated disc. They don’t know yet that they’ll need six months of physical therapy. They don’t know yet that their chronic headaches will require a neurologist. But the release doesn’t care what they know. It closes the door.

This is why gathering complete documentation before you sign matters so much:

- Medical records and specialist evaluations

- Imaging results (X-rays, MRIs, CT scans)

- Employer documentation of missed work and reduced capacity

- Bills, prescription receipts, and out-of-pocket expense records

- Written communications with the adjuster

Not because you’re building a lawsuit. Because you’re making a permanent financial decision and you deserve to make it with complete information.

Addressing the Worry Directly: “What If I’m Being Greedy?”

I hear this concern often. It’s doing real harm to real people, and I want to address it plainly.

Asking for time to understand your injuries is not greed. It’s basic financial literacy applied to a high-stakes decision. You wouldn’t sign a contract to sell your house three days after listing it, without an appraisal, because a buyer called quickly and sounded friendly. The same logic applies here.

The shame around negotiating an injury claim is, in my observation, partly manufactured. The framing that injured people are “lottery seekers” or “dragging things out” serves the interests of insurers who benefit from quick closes. The reality is that most people asking these questions just want to know they’re not leaving their family exposed to costs they can’t absorb.

Pausing is not aggressive. It’s not litigious. It’s not greedy. It’s what a careful person does when the decision is irreversible.

Two Paths: What the Outcomes Actually Look Like

The difference between signing early and waiting is not abstract. Here’s what it looks like in practice.

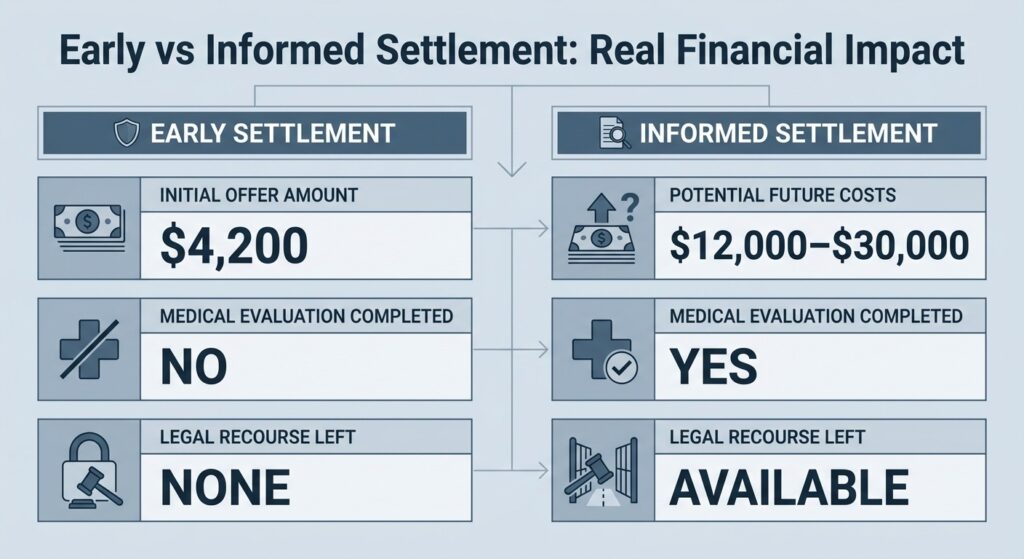

Path A — The Early Signature

You accept $4,200 on day three. You feel relieved. Two months later, your MRI shows a disc herniation. Your doctor recommends injections and possibly surgery. Your out-of-pocket exposure is $12,000 to $30,000 depending on your insurance. The claim release you signed means you have no recourse. The $4,200 is gone. The bills are yours.

Path B — The Informed Decision

You tell the adjuster you need time to complete your medical evaluation before discussing settlement. You see your primary care physician, get referred to a specialist, complete imaging. You gather your documentation. You consult a personal injury lawyer—not necessarily to file suit, but to understand what your claim is actually worth and what the release language means before you sign it. You make a decision with complete information.

The second path doesn’t require you to be adversarial. It doesn’t require litigation. It just requires that you treat this decision with the same care you’d give any other permanent financial commitment.

Consulting an attorney early doesn’t obligate you to anything. Most personal injury lawyers offer free initial consultations and can tell you quickly whether your situation warrants deeper review. If you’re outside Florida and navigating a similar situation, even a brief conversation with an accident attorney boston or wherever you’re located can clarify whether the offer you’ve received reflects your actual exposure.

Three Steps Before You Sign Anything

If you’re in that window right now—offer in hand, not sure what to do—here’s what I’d suggest.

1. Complete your medical evaluation first. Don’t let the settlement timeline drive your healthcare timeline. See your doctor. Get the referrals. Get the imaging. Let the clinical picture develop before you make a legal decision. This is the single most important step, and it’s the one most people skip because the adjuster’s call feels urgent.

2. Document everything, in writing. Medical records, bills, prescription receipts, pay stubs showing missed work, written communications with the adjuster. Documentation is what transforms a vague sense of harm into a substantiated claim. You need it whether you settle early or later—and gathering it costs you nothing but time.

3. Have one conversation with a personal injury lawyer before you sign. Not to start a lawsuit. Just to understand what you’re signing away, what your claim might actually be worth with complete information, and whether the release language is as broad as it usually is. That conversation costs you nothing and could protect you from a decision you can’t undo.

You are allowed to take time. You are allowed to ask questions. You are allowed to say “I need to understand this fully before I decide.”

That’s not delay. That’s exactly what a careful person does.